In mathematics, interest refers to the cost of borrowing money or the earnings from lending money, typically expressed as a percentage of the principal amount over time. There are two main types of interest:

- Simple Interest

- Compound Interest

Simple Interest

Interest on a loan or investment is traditionally calculated as simple interest, where principal refers to the amount borrowed. Because it does not include the compounding effect, which is clear and simple to follow. Simple Interest Formula:

Simple Interest (SI) = [P × R × T] / 100

Where:

- P is the principal amount

- R is the interest rate per annum

- T is the time in years

Example:

Let us look into and discuss an example to figure out the mechanism of simple interest. Assume the principal amount is $1,000 at 5% interest rate annually for 3 years. Using the formula:SI = [1000 × 5 × 3] / 100

= 150Therefore, the simple interest earned in 3 years is $150.

Applications

Common uses of simple interest in financial products include:

- Small-term loans - Primarily used for consumer and personal lending, home mortgages.

- Savings Account - Some of the savings accounts with banks provide simple interest.

- Bonds - Interest payments of certain bonds calculated on simple interest

Read More:Real-life Applications of Simple Interest

Compound Interest

Compound interest is based on the first principal and also on the added attractiveness of preceding periods. This method of interest compounding will make the investment or loan amount experience exponential growth. The compound interest formula is:

A = P(1 + r/n)nt

C.I. = A - P

Where:

- A is the amount of money accumulated after n periods, including interest.

- P is the principal amount.

- R is the annual interest rate.

- n is the no. of times interest is compounding per year.

- T is the time, the money is invested or borrowed for, in years.

Example: Assume principal amount be $1,000 with annually 5% interest compounded annually for the period of 3 years. Using the formula:

A = 1000(1 + (5/100))1 · 3

A = 1000 (1 + 0.05)3

A = 1000 × 1.157625

A = 1157.63

Applications

Compound interest is employed in almost every financial product such as:

- Savings Accounts: Increase savings over time with interest on the principal and compound.

- Manage investments: Grow wealth exponentially from compounding returns on equities, mutual funds, and retirement accounts.

- Mortgage: For mortgages, deal with home loan bad debts and expenses in the right way.

- Retirement Accounts: Future-proof income with the reinvested contributions and interest that has grown significantly.

Read More: Real-life Applications of Compound Interest

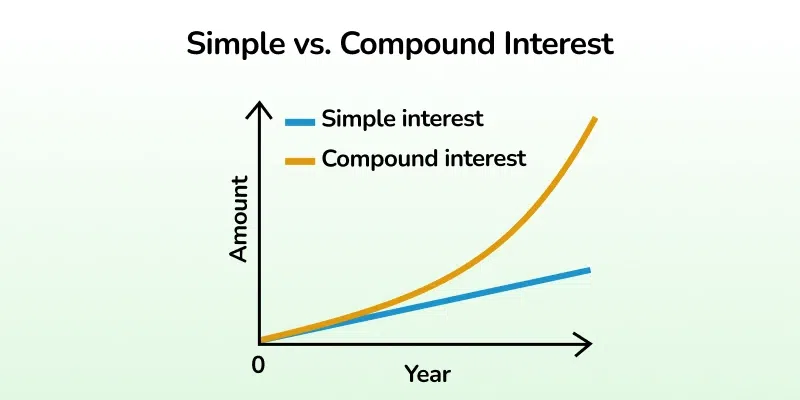

Comparing Simple and Compound Interest Using an Example

Let’s calculate and compare Simple Interest (SI) and Compound Interest (CI) for the given example:

- Principal (P) = $20,000

- Rate (r) = 10% (0.10)

- Time (t) = 4 years

Year | Simple Interest (SI) | Total Amount (SI) | Compound Interest (CI) | Total Amount (CI) |

|---|---|---|---|---|

1 | 2000 | 22000 | 2000 | 22000 |

2 | 2000 | 24000 | 2200 | 24200 |

3 | 2000 | 26000 | 2420 | 26620 |

4 | 2000 | 28000 | 2662 | 29282 |

For the first year, Simple Interest (SI) is equal to Compound Interest (CI) because no interest has been compounded yet. After the first year, Compound Interest starts growing faster due to interest being calculated on both the principal and the accumulated interest from previous years.

Difference Between Simple Interest and Compound Interest

To learn more about Simple Interest and Compound Interest study the table added below:

Aspect | Simple Interest (SI) | Compound Interest (CI) |

|---|---|---|

Calculation Basis | SI is only calculated on the principal amount. | CI is calculated on the principal amount plus the accumulated interest. |

Formula | S.I. = PRT/100 | C.I. = P(1 + r/100)n - P |

Growth Rate | Linear growth. | Exponential growth. |

Interest Earned | Lower interest earned compared to compound interest over the same period. | Higher interest earned due to the compounding effect. |

Applications | Short-term loans, some savings accounts, and certain bonds. | Long-term investments, savings accounts, and loans like mortgages. |

Example Calculation | For $1,000 at 5% per annum for 3 years: S.I. = $150 | For $1,000 at 5% per annum for 3 years (compounded annually): C.I. = $157.63 |

Interest Calculation | Interest isn't added back to the principal amount. | Interest is added back to the principal, leading to compound growth. |

Impact of inflation | Less effective in countering inflation. | More effective in countering inflation over time. |

Loan Repayment | The repayment amount remains constant over time. | The repayment amount can increase over time with compounding. |

Risk Factor | Lower risk due to straightforward calculations. | Higher risk due to variable growth potential. |

Solved Examples of Simple Interest and Compound Interest

Example 1: B borrowed $6000 from C, for 4 years at the rate of 2.5% per annum. Find the total interest earned by C at the end of 4 years.

Solution:

Given,

Principal (P) = $6000

Rate of Interest (R) = 2.5 %

Time (T) = 4 yearsSI = (P × R ×T) / 100

SI = (6000 × 2.5 × 4) / 100

SI = $600Therefore, the total interest earned by C at the end of 4 years is $600.

Example 2: What will be the compound interest on $2500 deposited for 2 years, compounded quarterly at interest of 4% per annum?

Solution:

Given,

Principal (P) = $2500

Rate of Interest (R) = 4%

Time (T) = 2 years, compounded quarterly:A = 2500(1 + (0.04/4))4 · 2

A = 2500 (1 + 0.01)8

A = 2500 × 1.082856

A = 2707.14Compound Interest = 2707.14 - 2500 = 207.14

Related Reads: