For any organisation, it is important to enjoy a sound and strong financial position. A sound financial position helps the business to meet up all the contingencies which can be anticipated or unanticipated. So, it is always preferable for the business to not distribute all the profits to the owners and rather some share of the profits should be kept aside by the businesses to meet any unforeseen liabilities that occur in the nearby future. The only way to make this possible is by making provisions and creating reserves out of the total profits that a business earns throughout the year.

Reserves

Reserves are nothing but a certain amount of the profits and surplus, which are kept aside to meet up the uncertainties in the future. Reserves are basically created to meet any unforeseen liabilities or losses that might occur in the future. Reserves are always created for specific purposes. Reserves can be utilized to buy any fixed asset, pay off dividends to the shareholders, for legal settlements, buy back shares, expansions, and many more. For any firm to enjoy the continuity or smooth flow of current business operations as well as to settle long-term liabilities, it is fundamental to create reserves. Following are some points that make the concept of reserves more understandable:

- Reserves are created out of divisible profits, not before calculating net profit.

- They are not a legal obligation (except certain statutory reserves).

- They are meant for unforeseen liabilities, not known obligations.

- They may be used for dividends, writing off losses, expansion, working capital needs, etc.

- If reserves are invested outside the business in securities, they are called a Reserve Fund.

- Reserves belong to the proprietors and are shown on the liabilities side of the Balance Sheet under Shareholders’ Funds.

Types of Reserves

1. Revenue Reserves

2. Capital Reserves

3. Specific Reserves

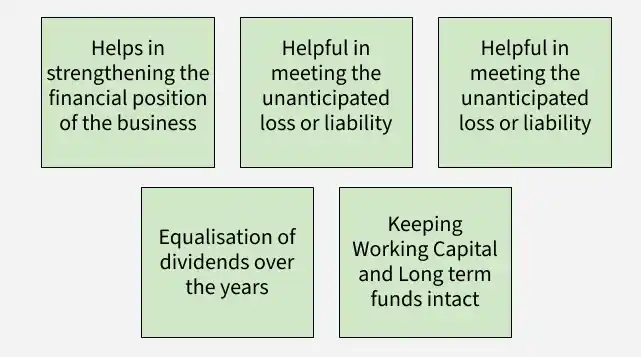

Importance of Reserves

- Strengthens Financial Position – Reserves increase the financial stability and net worth of the business. They improve creditworthiness and investor confidence.

- Meets Unforeseen Losses – They act as a safety cushion against unexpected losses or liabilities. This ensures business continuity during difficult times.

- Equalisation of Dividends – Reserves help maintain a stable dividend rate even when profits fluctuate. This builds goodwill among shareholders.

- Finances Expansion – Retained profits can be used for business growth, modernization, and asset replacement. This reduces dependence on external borrowing.

- Maintains Working Capital – Reserves help meet short-term financial needs and ensure smooth day-to-day operations.

Creation of Reserve

Reserves are never created out of the actual or net profits but rather created out of the divisible profits. The following illustration will explain how reserves are created.

Illustration:

There is a corporation named GFG Rollers Corp., and the main business of this corporation is to manufacture rollers and blades for industries for their production purposes. In the year 2021, GFG Rollers Corp. earned a profit of ₹2,35,000 through its business operations. The dividend pay-out ratio for the year 2021 has been decided at 30% to be paid to the shareholders. Also, the board of directors of the Corporation has proposed to keep aside 20% of net profits under the head of General Reserves. There already exists a fund for General Reserves with ₹10,000 in balance and a balance of ₹1,00,000 in Surplus. Find out the amount of Reserves and Surplus at the end of the year, 2021.

Solution:

i) For Dividend Reserve at the end of the year 2021,

Net Profits = ₹2,35,000

Dividend declared = 30%

Dividend Reserve = Net profits x Dividend payout ratio

Dividend Reserve =

Dividend Reserve = ₹70,500

ii) For General Reserve at the end of the year 2021,

Net Profits = ₹2,35,000

Opening General Reserve = ₹10,000

General Reserve = Opening Balance + % of net profits transferred to general reserves

General Reserve =

General Reserve = ₹10,000 + 47,000

General Reserve = ₹57,000

iii) For Surplus at the end of the year 2021,

Net Profits = ₹2,35,000

Opening Surplus = ₹1,00,000

Surplus = Opening Balance + Net profits - % of net profits transferred to general reserves - Dividend Reserve

Surplus = ₹1,00,000 + ₹2,35,000 - ₹47,000 - ₹70,500

Surplus = ₹2,17,500

For Reserves and Surplus at the end of the year 2021,

Reserves and Surplus = Dividend Reserves + General Reserves + Surplus

Reserves and Surplus = ₹70,500 + ₹57,000 + ₹2,17,500

Reserves and Surplus = ₹3,45,000

Thus, the total balance for the Reserves and Surplus at the end of the year 2021 stands at ₹3,45,000.