The Basis of Accounting describes the method by which the financial transactions and activities are accounted for and reported in the books of accounts to determine the profit or loss of any company. Profit earned or loss incurred by the business can be determined either by the Cash Basis of Accounting or the Accrual Basis of Accounting.

Cash Basis of Accounting

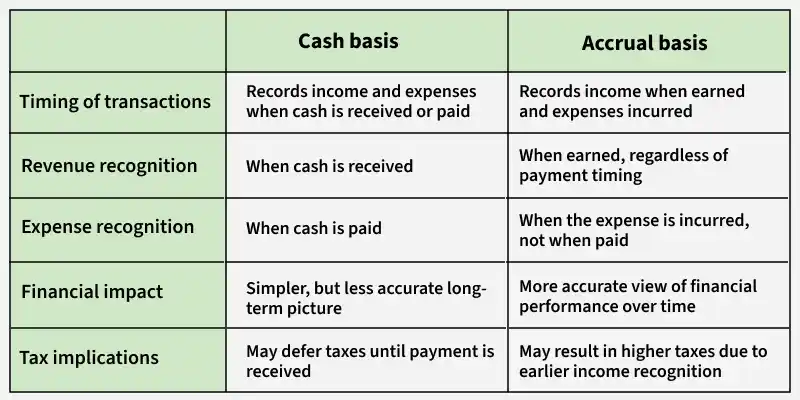

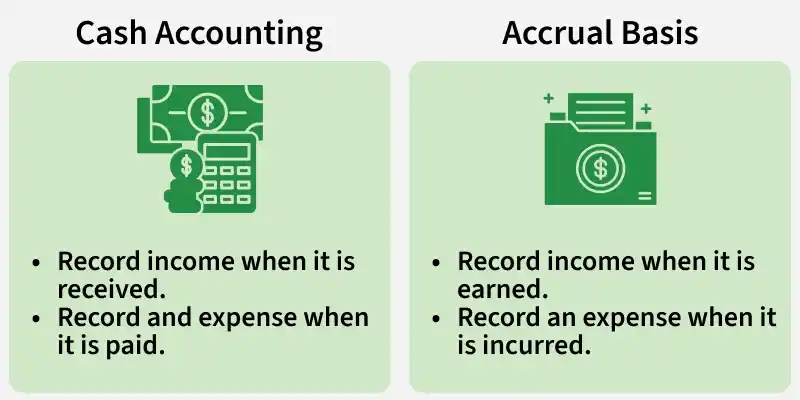

Transactions are recorded only when cash is actually received or paid, whether as revenue or expenses. It doesn't matter whether the amount which is received or paid belongs to the past, present or future year. Therefore, there is no possibility to record the credit transactions. Outstanding expenses and Accrued incomes are not recorded under the cash basis of accounting. Receipt and Payment Account prepared in the case of Not-for-Profit Organisations is an example of accounting on a cash basis. It is also called the Receipts basis of Accounting.

Key points of Cash basis of accounting:

- The accounting entries are only made when the actual payment or receipt has been made in cash.

- Credit transactions are not recorded in this method.

- Outstanding expenses and Accrued incomes are not recorded under this.

- Profit is the excess of receipts over cash payments.

- The cash payment in excess of the receipts is a loss.

Merits of Cash Basis of Accounting:

1. It is a very easy and simple method.

2. The conservative attribute of many entrepreneurs is satisfied with this method.

3. No personal estimates or judgments are required.

4. The profit and loss of a business can be easily calculated.

5. Better management of cash flow of the business owns

Demerits of Cash Basis of Accounting:

1. It does not give a true perspective of a company's profit or loss.

2. No adjustments related to outstanding expenses and accrued income is made, resulting in an incomplete view of financial statements.

3. There is more risk of account manipulation, as it does not record non-monetary items like depreciation, etc.

4. In the Court of Law, accounts prepared on an cash basis of accounting are not accepted as proof of evidence.

5. This method of accounting is not approved by the Companies Act 2013 and Income Tax department.

What is Accrual Basis of Accounting?

Accrual Basis of Accounting is a system where the transactions are recorded whenever they occur, no matter actual cash flow made or not. This means that the income is recorded when it is earned, regardless of whether it is due or received. Similarly, expenditure is recorded when it is due, irrespective of being due or paid. The profit or loss is the difference between the total expenses incurred and the income. This also called as Mercantile basis of accounting. Accrual basis of accounting is based on two basic accounting principles i.e. Matching Principle and Revenue Recognition Principle.

Key points of Accrual Basis of Accounting:

- The credit transactions are recorded in this.

- All the transactions whether cash is paid or not and received or not are recognised in this method.

- It is recognised by the Income Tax department and the Companies Act, 2013.

- Outstanding expenses, Income due, Income accrued and Prepaid expenses are all considered and recorded.

- Matching Principle and Revenue Recognition Principle of Accounting is applied in this method of accounting.

Merits of Accrual Basis of Accounting:

1. It shows the correct figures for profit and loss .

2. The final accounts under this method, reflect a complete picture of the financial position .

3. Non-cash items such as depreciation is recorded in this method.

4. The matching principle of accounting is followed in this method, which helps to calculate the exact loss or profit for the year.

Demerits of Accrual Basis of Accounting:

1. The use of estimates and personal judgements is required in this.

2. This basis of accounting is complicated, which requires more time, skill and resources.

3. This method of accounting can lead people to misinterpret financial statements.

4. The accounting process is too lengthy.

Cash vs Accrual