A compound journal entry is an entry that involves more than two accounts in a single transaction. It may include one debit and multiple credits, or multiple debits and one credit. This type of entry is used when a transaction affects several accounts at the same time. However, the total debits must always equal the total credits. Compound journal entries help record complex transactions clearly and efficiently.

Characteristics of Compound Journal Entries

- Multiple Accounts: Involves more than two accounts.

- Balanced: The total amount of debits must equal the total amount of credits.

- Complex Transactions: Used for recording transactions that impact several accounts at once.

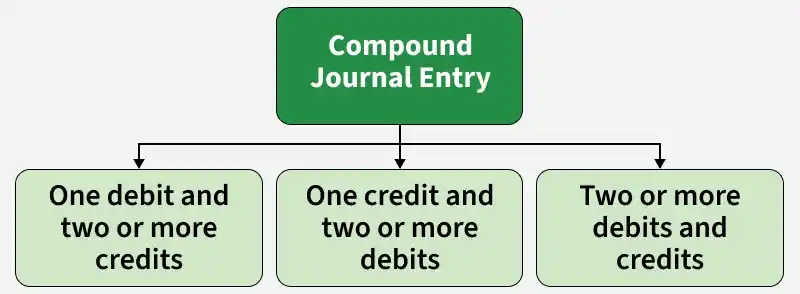

Compound Journal Entry Format

Examples of Compound Journal Entry

Example 1:

- 01 July 2022: Goods sold for cash 10,000.

- 01 July 2022: Cash received from Shubham 2,000.

- 01 July 2022: Received Rent of 8,000.

- 15 July 2022: Purchased Goods worth 20,000.

- 15 July 2022: Cash paid to Sahil 6,000.

- 15 July 2022: Commission paid of 4,000.

Solution:

Example 2:

- 01 June 2022: Paid Wages 2,000.

- 01 June 2022: Paid Advertisement Expenses 1,000.

- 01 June 2022: Paid Salaries 7,000.

- 10 June 2022: Received Interest 5,000.

- 10 June 2022: Received Commission 3,000.

- 10 June 2022: Received Dividend 2,000.

Solution:

When to Use Compound Journal Entries

- Combined Transactions: When a single transaction affects multiple accounts.

- Accruals and Prepayments: To record accrued expenses or prepayments that involve various accounts.

- Adjusting Entries: For adjusting entries that correct multiple accounts at the end of an accounting period.

- Complex Purchases: When purchasing multiple items or services that affect different expense accounts.

Advantages of Compound Journal Entries

- Efficiency: Saves time and effort by combining several transactions into one entry.

- Clarity: Provides a clear and concise record of transactions affecting multiple accounts.

- Accuracy: Reduces the risk of errors by consolidating related transactions.